With the passage of the Affordable Care Act, health care is now reported as part of your tax return. That means record keeping is even more important than ever. In years past people have switched plans and never even thought about the importance of keeping proof that they had the previous plan. From this point forward you will need to keep those old insurance cards right along with your tax receipts. If you are audited by the IRS, proof of insurance will need to be given just like your W-2. According to the IRS website: “keep records for three years from the  date you filed your original return or two years from the date you paid the tax, whichever is later, if you file a claim for credit or refund after you file your return.” * Certain exceptions apply for record keeping. See www.irs.gov for more details or contact us. Remember to keep a file for medical expenses.

date you filed your original return or two years from the date you paid the tax, whichever is later, if you file a claim for credit or refund after you file your return.” * Certain exceptions apply for record keeping. See www.irs.gov for more details or contact us. Remember to keep a file for medical expenses.

If you itemize your deductions for a taxable year on Form 1040, Schedule A, you may be able to deduct expenses you paid that year for medical and dental care for yourself, your spouse, and dependents. For more information, see Questions and Answers: Changes to the Itemized Deduction for 2014 Medical Expenses on www.IRS.gov.

Category: Uncategorized

New Rules on the Horizon for Medicare Cards

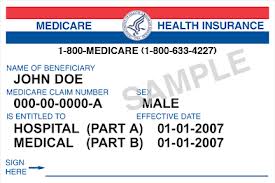

It is official and about time! Medicare will no longer use your Social Security number on your Medicare card. I have been telling people for years not to carry their Medicare card unless necessary since it contains your Social Security number. With feedback from providers and the spike in identity theft, Medicare has decided that it makes sense to change the current practice.  The change is coming a bit late compared to the rest of the industry. Private insurance companies no longer use Social Security numbers to identify card holders, and the federal government has also forbidden insurers from using the numbers on insurance cards when medical or drug benefits are provided through Medicare contracts.

The change is coming a bit late compared to the rest of the industry. Private insurance companies no longer use Social Security numbers to identify card holders, and the federal government has also forbidden insurers from using the numbers on insurance cards when medical or drug benefits are provided through Medicare contracts.

This new change will take time to implement. Medicare has up to four years to start issuing the new cards, and four more years to reissue current cards.

Healthcare Paperwork: Is yours in order?

Healthcare distortion can involve a host of medical and legal complications. At best, these issues may affect you financially; at worst, they could mean the difference between life and death. Whether you go to the hospital for a routine procedure or for an emergency, there are  steps you can take to help avoid complications.

steps you can take to help avoid complications.

- Is your Medical POA or Advanced Medical Directive (“Living Will”) up to date?

- Make sure your name and all other personal information is completely accurate at each doctor’s appointment, outpatient surgery, and/or hospitalization.

- Have you read and do you understand your health insurance coverage?

- Are you saving documents and bills you receive regarding your health care?

- Does your personal representative have current copies of your directives and documents?

Educational event at Woodhead Insurance July 18th at 10am — come learn more RSVP

Is retirement in your near future?

Woodhead Insurance, in partnership with Hellenbrand Financial, is hosting an event on July 14th and 16th at NWTC. This informative event is meant to help people learn what they need to know as they head into retirement.

It will teach attendees:

Basics of Medicare:

How to enroll

How it works

What it covers

When to sign up

When to delay enrollment

Retirement 101:

Social Security – How to get maximum benefits

Annuities – The different types, the positives and negatives of each

Long Term Care – Learn how different programs work, and about new “hybrid” options

This event is free and open to the public. It is not a sales pitch and there is no obligation. Space is limited, however, so your reservation is required. Please call the office at (920) 544-0058 to RSVP.

News from the Woods

With the weather finally warming here in Wisconsin, Spring brings a time of change. At Woodhead Insurance, we would like to remind you of the importance of notifying us of any life changes you may have. Changes in your life can have an effect on many things, including insurance. Notifying us of these life changes allows us to make sure your health insurance continues to serve you. If you are not sure, call us at 920-544-0058! We’d love to hear from you and celebrate life’s milestones together. Remember we don’t always receive your notices so you have to let us know if you want us to help.

As your advocates, we want to make sure your benefits are protected and that updates are made promptly and accurately. Ensuring you get the most bang for your insurance buck, we offer a host of products around health insurance such as: accident policies, funeral trusts, simple life insurance, dental coverage, and a legal protection plan. You already know we don’t pressure anyone to purchase our products. A good product does not require a pushy salesperson, so feel free to give us a call and, “Window Shop” any of our products. Find out the benefits and costs so you can make your own decision. Being an independent agent, we have a vast network of reputable companies and products. If we don’t carry what you need, we can recommend a reputable and trustworthy provider to assist you. Happy Spring! Diane Woodhead

Healthcare Legal Tips

Not preparing for healthcare concerns can involve a whole host of medical and legal complications. At best, these issues may affect you financially; at worst, they could mean the difference between life and death. Whether you go to the hospital for a routine procedure or an emergency, there are steps you can take to help avoid complications.

- Have an up-to-date Medical Power of Attorney or Advanced Medical Directive (“Living Will”).In the event you cannot make medical decisions yourself, these documents entrust decisions about your care to a person you designate. Advise your family of your designation so that person is notified when decisions must be made.

- Make sure your name, identifying information and all other information is completely accurate at each doctor’s appointment, outpatient surgery and hospitalization. Serious problems involving medical care sometimes begin as simple clerical errors. A small error can create a major treatment crisis. Reduce the chance of error by carefully reviewing all of your doctor’s office or hospital admissions paperwork. During hospitalization check your hospital wristband for errors. I know this may sound cheeky but read the documents you are signing.

- Understand your health insurance coverage before you get sick. It is important that you understand all of the limitations and exclusions in your insurance policy. Your policy may require you to obtain preauthorization for medical procedures. In addition, you may need supplemental coverage or disability coverage in the event of a long recovery. Review your health coverage now. It is too late to make critical changes after you get sick. If you have questions about your policy reach out to us as we are here for you!

- Save any documents you receive regarding your care or billing. Retain all of your medical documentation in the event of a fee dispute, insurance dispute or medical malpractice claim. Documents can be easily misplaced in the confusion of care and recovery. If you are too ill to organize your own paperwork ask someone you trust to help manage your documentation. It is also a great idea to keep a running journal of the dates of service and procedure’s done. If you call regarding a bill it doesn’t hurt to document who you spoke to, when you spoke to them and what information was received.

- Ask for a second opinion if you are unsure about your diagnosis or treatment. You always have the right to speak with another doctor or caregiver if you are uncomfortable with the diagnosis or treatment recommendations being made. If someone wants you to have an expensive procedure or treatment make sure to be the smart consumer who asks lots of questions.

- Advocate for your own quality care! It is important to speak up for yourself in healthcare situations. If you or a loved one have been hospitalized and have concerns about the quality of care, speak to a doctor or nursing supervisor. If you are unable to advocate for yourself due to the nature of your illness, medications or treatments, have a friend or family member stay with you. Many hospitals have a designated advocate on staff. If you feel your concerns are not addressed ask to speak with a patient advocate.

What YOU Should Know About Estate Recovery in Wisconsin

Some important changes are taking place in the Estate Recovery Program as a result of the 2013-2015 biennial budget that was passed by the Wisconsin State Legislature in 2013. These changes will begin August 1, 2014.

Some important changes are taking place in the Estate Recovery Program as a result of the 2013-2015 biennial budget that was passed by the Wisconsin State Legislature in 2013. These changes will begin August 1, 2014.

Background

Through the Estate Recovery Program, the state seeks repayment for the cost of certain long term care services paid for by Medicaid and BadgerCare Plus, and all services paid for by the Wisconsin Chronic Disease Program (WCDP). Repayment is made from the member’s property after they pass away or from liens placed on their homes. The money recovered from the member’s estate is returned to the program and used to pay for care for other members. It is important to remember that the state does not seek repayment from a member’s property while the member is survived by a:

- Spouse

- Child under age 21

- Disabled or blind child of any age.

Repayment is made only after the member or the surviving spouse passes away or, in some situations, from a lien on the member’s home. Liens are not filed against homes of members while they are living in the community. The Estate Recovery Program is paid after certain other expenses are paid according to standard probate procedures. Costs paid prior to the Estate Recovery Program include:

• The costs of administering the estate, including attorney fees.

• Reasonable funeral costs.

• The costs of the last illness, if any, that were not paid by Medicaid, BadgerCare Plus, or WCDP.

Policy Changes

Beginning August 1, 2014, certain new assets and services will now be part of the Estate Recovery Program.

The assets below will now be part of the Estate Recovery Program:

• Joint Tenancy Property

Repayment will be made after the member passes away from joint tenancies created on and after August 1, 2014. Repayment will be made from the interest in the property that the member has at the time the member passes away. Tax Equity and Fiscal Responsibility Act of

1982 (TEFRA) liens will continue to be filed on joint tenancy homes and repayment will be made from joint accounts at financial institutions, no matter when the joint tenancy was created.

• Life Estates

Repayment will be made from a life tenant’s interest in life estates that are created on and after August 1, 2014.

• Life Insurance Policies

Repayment will be made from a member’s life insurance policy, no matter who is named as the beneficiary, for life insurance policies created on and after August 1, 2014.

• Marital Property

Repayment will be made from 50 percent of the surviving spouse’s estate.

• Revocable Trusts

Repayment will be made after the member passes away from revocable trusts created on and after August 1, 2014. A TEFRA lien will continue to be filed on a home in revocable trust regardless of when the trust was created.

• Tax Equity and Fiscal Responsibility Act of 1982 Liens

Repayment will be made through TEFRA liens placed on life estates that are created on and after August 1, 2014.

• Other Non-probate Property

Repayment will be made from non-probate property not listed above for any member who passes away on or after August 1, 2014. These assets will be used as repayment for members who pass away on and after August 1, 2014.

Services

The cost of the services below will now be included in the amount that the Estate Recovery Program will seek repayment for:

• All services received while participating in a long term care program

Repayment will be made for all services received on and after August 1, 2014, by a member age 55 years and older participating in a long term care program. This

includes members participating in home and community-based waiver programs, and the Program of All-Inclusive Care for the Elderly (PACE).

• Capitation payments

Repayment will be made for the entire capitation payment made to a managed care organization (MCO) beginning August 1, 2014, for a member participating in a long term care program. Repayment of these services applies to services received and capitation payments made on and after August 1, 2014, for any member age 55 and older participating in a long term care program. Long term care programs include all home and community-based programs and PACE.

Program Dis-enrollment

Members should contact the source listed below for their program before July 18, 2014, for benefit counseling if they do not want the new services recovered and will need to dis-enroll from their program. This will allow for case closure and dis-enrollment from Wisconsin Medicaid, BadgerCarePlus, or WCDP prior to the new rules taking effect:

• Medicaid — Contact your local Aging and Disability

Resource Center (ADRC).

• BadgerCare Plus — Contact your agency.

• WCDP — Contact Member Services at 1-800-362-3002.

For More Information

http://www.dhs.wisconsin.gov/publications/p1/p13032-C.pdf

ACA Subsidies Challenged in Courts

You may have seen or heard two stories in the news about two conflicting federal court decisions regarding the legality of federal subsidies for low- and middle-income people who bought health insurance through the Federally Facilitated Marketplace (FFM), or Exchange, in certain states, including Wisconsin.

Woodhead Insurance wants all of our members to know that their health plans are safe and they are still covered. Premiums are not going to change at this time.

You may assure that we will continue to closely monitor the situation. If you have any questions please feel free to call us at 920-544-0058

Sincerely,

Diane Woodhead

As always we strive to not only be your agent but also your health insurance advocate.

May is National Stroke Awareness Month

Know the warning signs

Know the warning signs

It’s important to learn the warning signs of stroke. Use FAST to remember the warning signs:

FACE:

Ask the person to smile. Does one side of the face droop?

ARMS:

Ask the person to raise both arms. Does one arm drift downward?

SPEECH:

Ask the person to repeat a simple phrase. Is speech slurred or strange?

TIME:

If you observe any of these signs, call 9-1-1 immediately.

Heart disease and stroke prevention

• Physical activity

• Healthy eating

• Know your numbers: Blood pressure, cholesterol (total, HDL, LDL, and triglycerides), and blood sugar levels

These tests are covered as part of your yearly physical at no cost to you. Prevention saves lives and money!

Do Not Call Registry

What’s a Robocall?

What’s a Robocall?

If you answer the phone and hear a recorded message instead of a live person, it’s a robocall. You’ve probably gotten robocalls about candidates running for office, or charities asking for donations. These robocalls are allowed. But if the recording is a sales

message and you haven’t given your written permission to get calls from the company on the other end, the call is illegal. In addition to the phone calls being illegal, their pitch most likely is a scam.

What’s the Reason for the Spike in Robocalls?

Technology is the answer. Companies are using auto-dialers that can send out thousands of phone calls every minute for an incredibly low cost. The companies that use this technology don’t bother to screen for numbers on the national Do Not Call Registry. If a company doesn’t care about obeying the law, you can be sure they’re trying to scam you.

What Should You Do If You Get a Robocall?

If you get a robocall:

• Hang up the phone. Don’t press 1 to speak to a live operator and don’t press any other number to get your number off the list. If you respond by pressing any number, it will probably just lead to more robocalls.

• Consider contacting your phone provider and asking them to block the number, and whether they charge for that service. Remember that telemarketers change Caller ID information easily and often, so it might not be worth paying a fee to block a number that will change.

• Report your experience to the FTC online at or by calling 1-888-382-1222.

What Prerecorded Calls Are Allowed?

Some prerecorded messages are permitted — for example, messages that are purely informational. That means you may receive calls to let you know your flight’s been cancelled, reminders about an appointment, or messages about a delayed school opening. But the business doing the calling isn’t allowed to promote the sale of any goods or services. Prerecorded messages from a business that is contacting you to collect a debt also are permitted, but messages offering to sell you services to reduce your debt are barred.

Other exceptions include political calls and calls from certain health care providers. For example, pharmacies are permitted to use prerecorded messages to provide prescription refill reminders. Prerecorded messages from banks, telephone carriers and charities also are exempt from these rules if the banks, carriers or charities make the calls themselves.

http://www.consumer.ftc.gov/articles/0259-robocalls

Please visit the FCC website for more information