IRMAA is an acronym for Medicare’s Income-Related Monthly Adjustment Amount (IRMAA). This is a higher premium charged by Medicare Part B and Medicare Part D to individuals with higher incomes.

Social Security uses the most recent tax return provided by the IRS. This means that the IRMAA determination ends up being based on a tax return from two years ago. For example, the 2020 IRMAA determination is based on 2018 tax return.

The number used is the Modified Adjusted Gross Income (MAGI) and it is a sliding scale. The sliding scale currently starts at $85,000 for individual income and $170,000 for married filing jointly income.

Unlike late enrollment penalties, which can last as long as you have Medicare coverage, IRMAA is calculated every year. You may have to pay the adjustment one year, but not the next if your income falls below the threshold.

So if you will be starting Medicare in the next few years make sure are aware of this increase to your costs. Let us know if you have any questions.

Below are links to Medicare’s website that has the charts for what you will pay for part B and part D premiums.

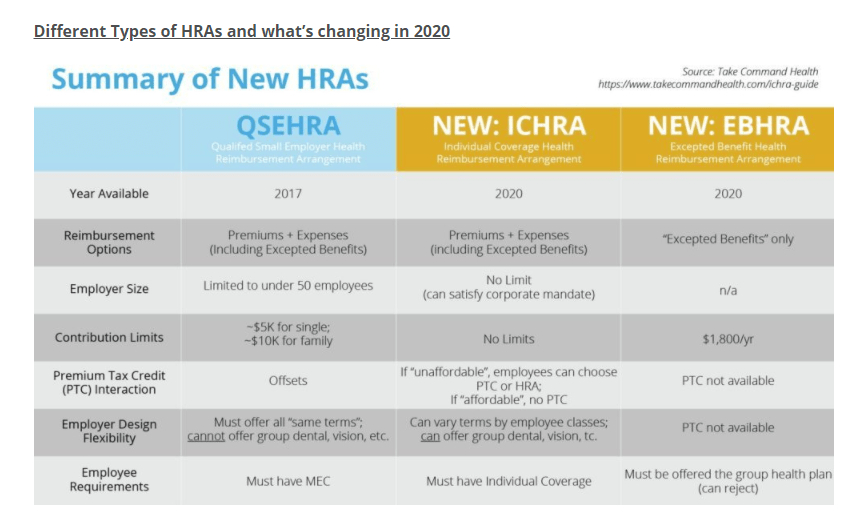

Changes have been made to make this a more enticing option. Health Reimbursement Arrangements (HRAs), an employer-funded benefits option since the 1970s, will undergo an extensive transformation beginning in January 2020.

An HRA is a type of benefits arrangement in which employers reimburse employees for health insurance expenses like monthly premiums, deductibles, and out-of-pocket medical costs. Both sides of this agreement receive tax benefits, as businesses can claim a tax deduction for the reimbursements and employees are reimbursed for eligible expenses tax-free.

This allows the employer to help fund the cost of healthcare but not take on the administration of the benefits. It gives the employee more freedom to choose a plan that works with their provider of choice, but to ensure that the employee understands the plan and benefits, it is helpful to work with an agent. The health insurance agent will educate and assist your employee to find the right plan for them.

It is not right for all businesses or all employees and there can be pit falls that you will need to comprehend prior to making this decision. Employees cannot use tax credits for health insurance and get employer sponsored payments. For some employees this would push them to higher deductibles. An evaluation would need to be done by an agent. Woodhead Insurance Services LLC is here to help.

Individual Coverage Health Reimbursement Arrangement (ICHRA): In June 2019, the Trump administration finalized new HRA rules that will create two new types of HRAs for 2020. ICHRA, like QSEHRA, will enable businesses to reimburse employees for premiums and other qualified expenses, but there are key differences between the two. ICHRA regulations include the following core features:

Businesses of any size will be eligible to offer ICHRAs.

No restrictions on the annual amount employers may reimburse employees.

Businesses may offer varying terms, and reimbursement allotments, to different employee classes (such as full-time, part-time, seasonal, non-salaried, etc.).

ICHRAs enable large employers to fulfill the Affordable Care Act’s employer mandate, which requires them to offer affordable, minimum essential health coverage to at least 95 percent of their full-time employees.

ICHRA terms must remain uniform among employees of the same class, except that businesses may alter allotments based on the employee’s age or the number of dependents. ICHRA contributions, in order to satisfy the employer mandate, must provide employees an opportunity to purchase “affordable” individual market plans. According to the IRS, an ICHRA is considered affordable if “the remaining amount an employee has to pay for a self-only silver plan on the exchange is less than 9.86% of the employee’s household income.”

ICHRA beneficiaries must maintain individual health coverage, through purchasing on-exchange or off-exchange insurance plans.

Excepted Benefit Health Reimbursement Arrangement (EBHRA): Also coming to the 2020 HRA environment are EBHRAs, another component of the recent Trump administration directive. EBHRAs allow employers to contribute up to $1,800 per year toward their employees’ expenses that are not covered by their group plan. These types of HRAs can be used to reimburse employees for expenses such as short-term insurance and dental, vision and home care, among other certified costs. Under EBHRA regulations, these employers must also offer a group health plan.

How will the new HRA landscape — particularly the arrival of ICHRA — impact employers and employees? What about HR platforms and InsurTech companies?

It’s expected that the new HRA rules, especially the availability of ICHRAs, will transform the employer-sponsored health insurance market by transitioning employees from group plans to the individual market. For employers, this lessens their administrative burden. For employees, this means more personal choice and greater control of their insurance options.

With more businesses eligible to offer HRAs, it’s likely the individual market will grow substantially over the next few years. And, millions of employees will experience shopping for and enrolling in on-exchange and off-exchange individual plans for the first time.

According to a U.S. Departments of Health and Human Services, Labor, and the Treasury estimate, it will take employers around five years to fully adjust to the updated rule, at which time roughly 800,000 businesses will offer ICHRAs. This, the departments’ modeling suggests, will cover about 11 million employees and family members.

The White House calculates that, as an effect of the new directive, the size of the individual market could increase by as much as 50%.

Woodhead Insurance Services it here to help you with your employee needs as they shop for a plan for themselves or their families. Call us today to learn more. 920-544-0058

Your health and wellbeing are our number

one priorities at Woodhead Insurance Services LLC. We want to make sure you

have the information and resources you need to stay safe. I have discussed with some of you the benefit of

virtual visits, but want to reiterate the value of not going where sick people

are. Maybe it is time to reschedule your wellness check or at least call the doctor’s

office to see if they want you to come in.

It is also time to familiarize yourself with your options for care. Here are the links for each insurance company’s virtual visits. I have personally used this and can verify that it was very easy and we are here to help you if you need us. Many of the below plans offer this to members for free. Most plans are offering COVID-19 testing for no cost, but check their site or call/email us with questions. If you need to speak with someone due to anxiety… the lines are here to help you too!

Nurse

Line / Care My Way for Security Health Plan members: 1-800-549-3174. Most

Security Health Plan members have unlimited access to Nurse Line or Care My Way

services for free.

UnitedHealth

care

Speak

to network telehealth providers using your computer or mobile device online at www.amwell.com

NOW

AVAILABLE – directly with your current clinic (((co-pays may apply)))

Ascension Online Care is also offering video urgent care

visits at a discounted rate of $20, valid through March, so you can talk to a

doctor from home. No insurance required. Use the code HOME at Ascension Online

Care

Nutrition is an important part of living a healthy lifestyle and it has become a growing trend in our nation to not only eat better but to support our local farmers and businesses. Eating unprocessed foods is a great way to make a change in your eating habits.

In our area farmer’s markets have become very popular and are not held just on the weekend any longer. The days of a farmer’s market just having a few food stalls is mostly in the past, now you can find a wide range of goods from clothing to bird feeders and household items. Farmer’s markets have even become a place to socialize; stretch your legs and take a stroll through the vendor stands, stop and listen to a local musician or catch up with a friend and enjoy the welcoming atmosphere!

Not sure where to start? Below are a few of the local options you can find for farmer’s markets.

Did you know that if your employer group plan is small, delaying the Part B enrollment could create a penalty?

When you are eligible for Medicare usually at 65 you are required to maintain creditable coverage or enroll into the Medicare program with parts A, B, & D. In most situations employer group is considered creditable and you can delay the enrollment and stay on the group plan, but not always.

You may want to wait to sign up for Medicare Part A (hospital service) and/or Part B (outpatient medical services) if you are working for an employer with more than 20 employees when you turn 65, and have healthcare coverage through your job or union, or through your spouse’s job. COBRA is not considered employer group coverage.

*If you are disabled under 65 and working (or you have coverage from a working family member), the Special Enrollment Period rules also apply as long as the employer has more than 100 employees.

When deciding to delay your Medicare enrollment it is important to determine if you will qualify for Special Enrollment Period (SEP).

You can get a Special Enrollment Period to sign up for Parts A and/or B:

• Any time you are still covered by the employer or union group health plan through your or your spouse’s current or active employment, OR

• Within 8 months following the month the employer or union group health plan coverage ends or when the employment ends (whichever is first).

If you wait longer, you may have to pay a penalty when you join.

When in doubt it is important to schedule an appointment with the local social security office and have them assist you in making the best decision for you.